Following a Strong 2021, 2022 Has Been a Tough Year For the Global Economy

Coming off a strong year for corporate earnings and economic growth in 2021, the global economy has been hit with myriad headwinds in 2022. The unfathomable sequence of events occurring in Ukraine is certainly top of mind. Beyond the horrific human tragedy, there has been a significant ripple effect on global commodity prices. This has added to already mounting inflationary pressures from ongoing supply chain problems and has led central banks around the world to expedite their rate hike plans in an attempt to get inflation under control.

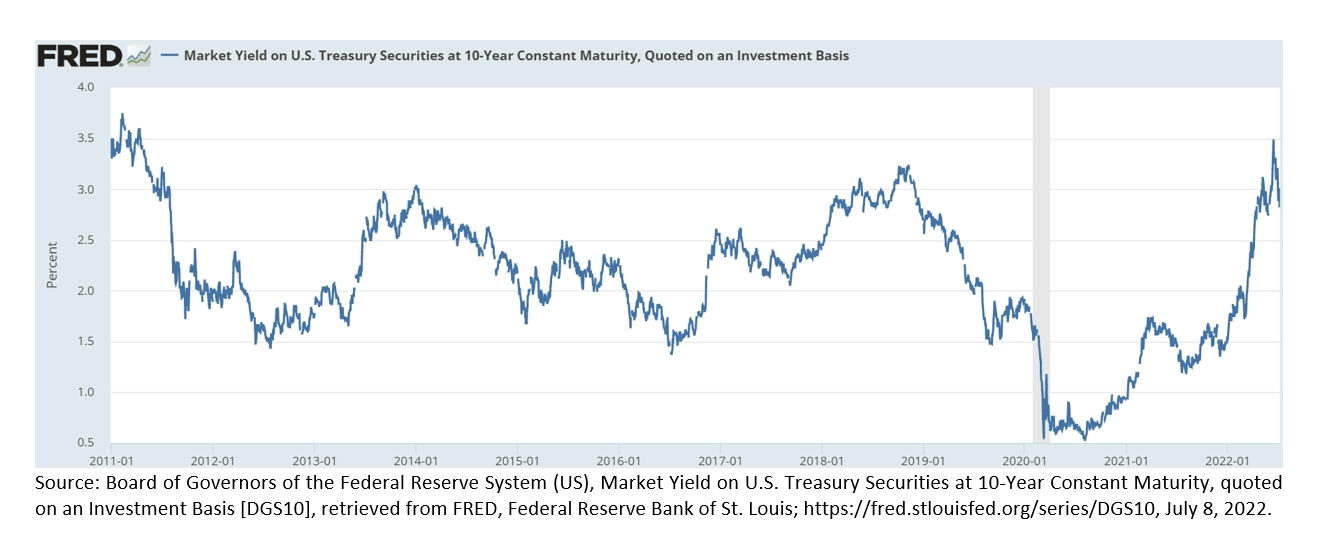

As a result, interest rates in the U.S. and globally have increased dramatically. Coming into the year, the 10-year U.S. Treasury rate was 1.52%. On June 15, 2022, the Federal Reserve announced a 75-basis point hike in rates, leading the 10-year yield to skyrocket as high as 3.49%, its highest level since the second quarter of 2011. This was the largest single increase in the federal funds rate since 1994. While rates are still well below long-term historical levels, this marks only the third time in the last decade we have experienced yields above 3% on the 10-year. The two previous occurrences were relatively short lived, as rates gradually moved back below 2%.

How has the current interest rate environment impacted bond investors? Interest rates have a direct impact on bond pricing. When interest rates rise, bond yields also typically rise. As investors look for higher yielding bonds, the demand for the existing lower yielding bonds decline, leading the price of these bonds to ultimately fall. This is exactly what has happened in 2022. Interest rates have increased dramatically, leading to significant price declines and historically poor returns to start the year. The Bloomberg U.S. Aggregate Index is down ~11% through June 24, 2022, marking the worst start to a year for bond returns on record.

What can investors expect, going forward? Based on the current environment and the possibility of continued rising rates, some may start to question their fixed income allocation. While this may be enticing, we believe it is best to stay the course and maintain long-term allocations to fixed income. Below are a few things that investors should be thinking about when looking at their bond portfolio.

Loss of Principal

As painful as fixed income performance has been to start the year, it is important to remember that the price declines or “losses” are only temporary. So long as the underlying bonds do not default, the price will move towards par value as the security gets closer to maturity. For long-term investors not forced to sell their fixed income holdings at a loss, the principal amount should be recovered over time.

Valuations Looking Better

We believe the current environment could represent a buying opportunity, as fixed income valuations and yields are looking increasingly attractive. As bad as the performance has been over the last year, there could be some positives when looking ahead. Higher interest rates mean that investors will earn higher yields form their bond portfolio, providing more protection against rising rates. History shows that previous poor performance periods in bonds have typically been followed by strong 12-month returns, as indicated in the chart below.

Higher Yields and Return Expectations

What if rates continue to move higher? While this might cause bond prices to dip in the short-term, the proceeds from maturing bonds will be reinvested in higher yielding new issues. This will lead to more income generation for investors, an important factor for those relying on income from their portfolios, and ultimately increase return expectations going forward. Historically, starting yields have been a very strong indicator of future fixed income returns.

When faced with the potential of sustained rising interest rates and elevated inflation, some investors may feel the need to make significant changes to their bond portfolios or even eliminate the asset class all together. Rather than trying to drastically change portfolio positioning or make bets on future interest rate movements, we recommend strong diversification within a fixed income portfolio. Exposure to different parts of the yield curve – both short term and intermediate term – and to varying sectors, geographies, and credit quality can help ease volatility. Holding both fixed and floating rate structures can further help smooth investor returns over time. Bonds continue to serve an important role in portfolios, providing diversification, liquidity, and downside protection for investors during recessionary periods.

Sources:1U.S. Bonds represented by the IA SBBI US GOV IT Index from 1/1/26 to 1/3/89 and the Bloomberg U.S. Agg Bond TR Index from 1/3/89 to 4/30/22. About the Author:Steven Fraley is a Vice President and Consultant at Innovest. He provides consulting services to retirement plans, nonprofits, and families. Steven is a member of the Innovest Investment Committee, which drives the firm’s investment related research and due diligence. He is also a member of the Due Diligence Group, responsible for independently sourcing investment managers, as well as monitoring recommended products and strategies. The group utilizes both quantitative and qualitative analysis evaluating performance, understanding return attribution, and meeting management teams both at Innovest and at their offices. The group works in conjunction with Innovest’s Investment Committee. Steven is also the Director of Innovest’s Capital Markets Research Group, responsible for monitoring the global macro-economic environment, asset allocation modeling and portfolio construction. Disclosure:Innovest is an Associate Member of TEXPERS. The views and opinions contained herein are those of the author and do not necessarily represent the views of Innovest nor TEXPERS. These views are subject to change.