TEXPERS invited two experts with Putnam Investments, an Associate member of the association, to discuss inflation expectations. Shep Perkins, CFA, is Chief Investment Officer of Equities at Putnam and Donald E. Perks is a Quantitative Analyst with the firm.

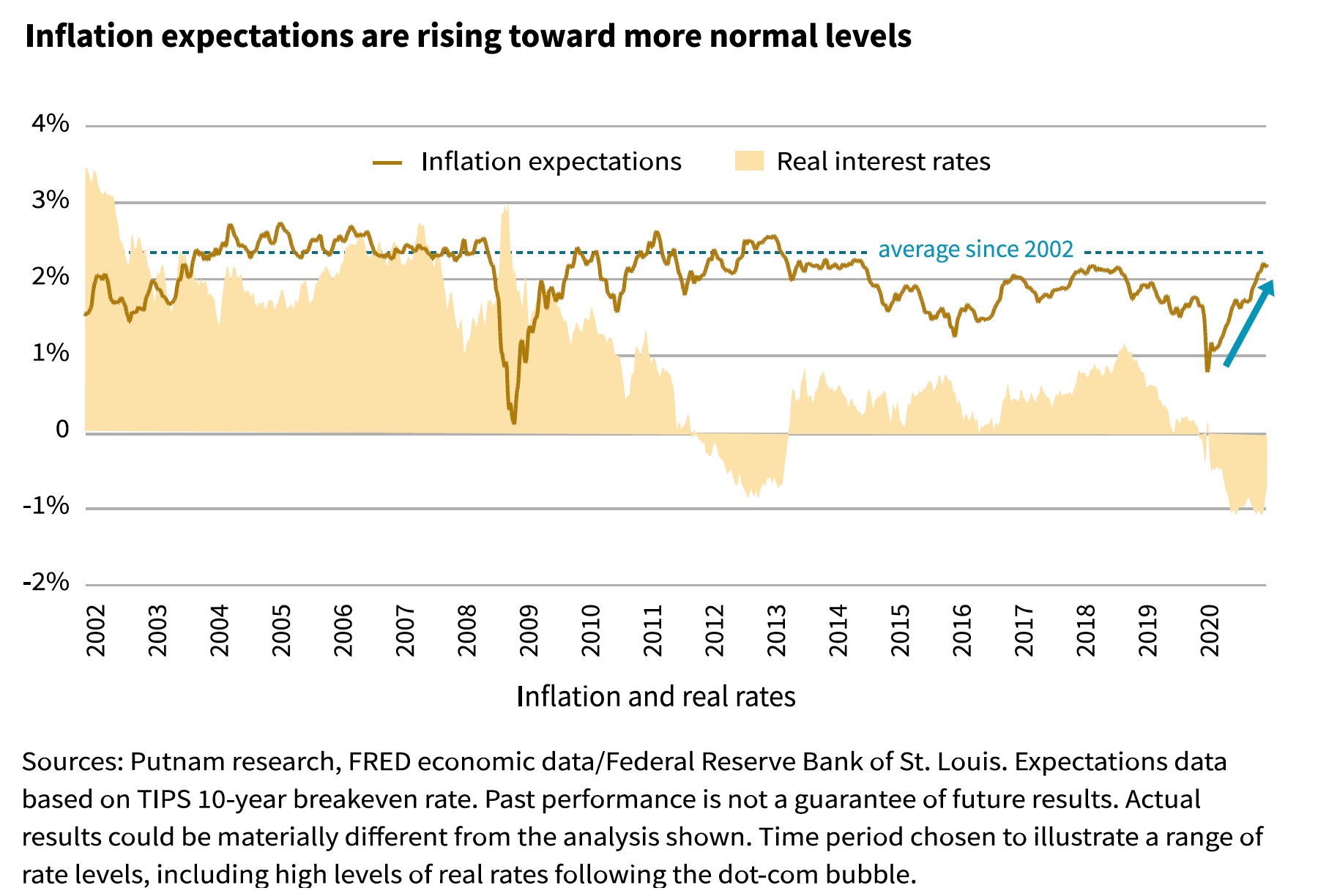

SHEP: A few quarters ago, the idea of an overheating economy was unimaginable to most investors. In recent months, however, a lot has changed. The distribution of three effective Covid-19 vaccines is well under way, the U.S. economy registered growth above 4%, and we see growing optimism about a return to normal. Commodity prices are at multiyear highs, and personal income is rising.

In this environment, we are seeing a sharp uptick in inflation expectations. In 2020, historically low interest rates were key to helping equity markets soar despite the pandemic. Today, some stocks are struggling, and equity investors have become more cautious as the 10-year Treasury yield reached its highest level in more than a year.

We believe that rising inflation will not dampen equity market performance; history has shown that rising inflation has generally been followed by strong equity returns.

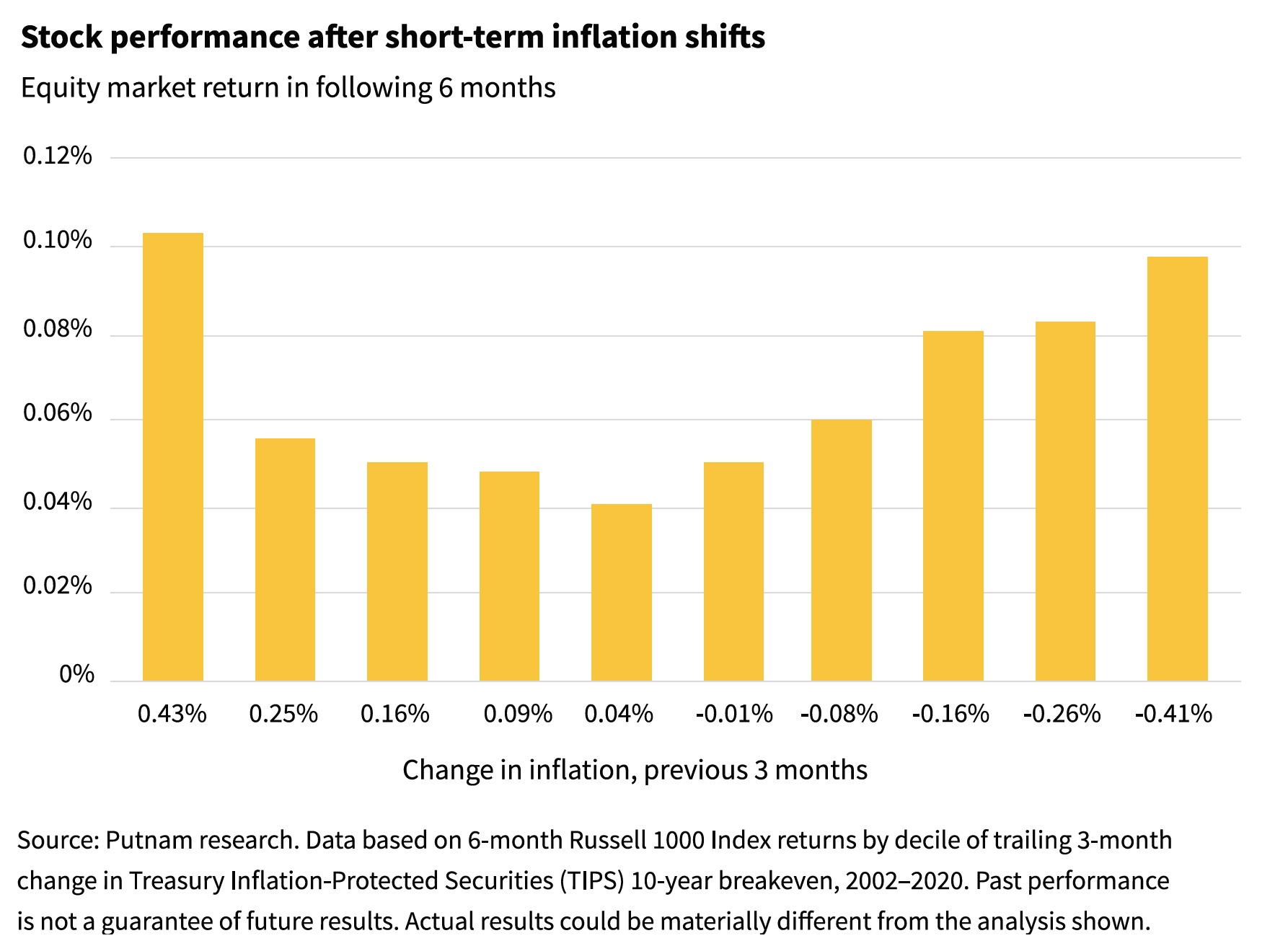

How has the market responded to inflation?

DON: We analyzed changes in inflation during 3-month periods over the past 18 years. We then looked at how the equity market performed in the following six months. Returns for stocks were better after the periods in which inflation increased or decreased the most, as a modest increase in inflation was typically accompanied by a strengthening economy, providing a positive backdrop for corporate earnings growth.

SHEP: On the flip side, when inflation decreased the most, stocks also delivered better returns. This deflationary environment is also positive for equities because it typically follows aggressive monetary and fiscal stimulus.

In our view, stocks are poised to deliver positive returns in the coming months despite the uptick in inflation.

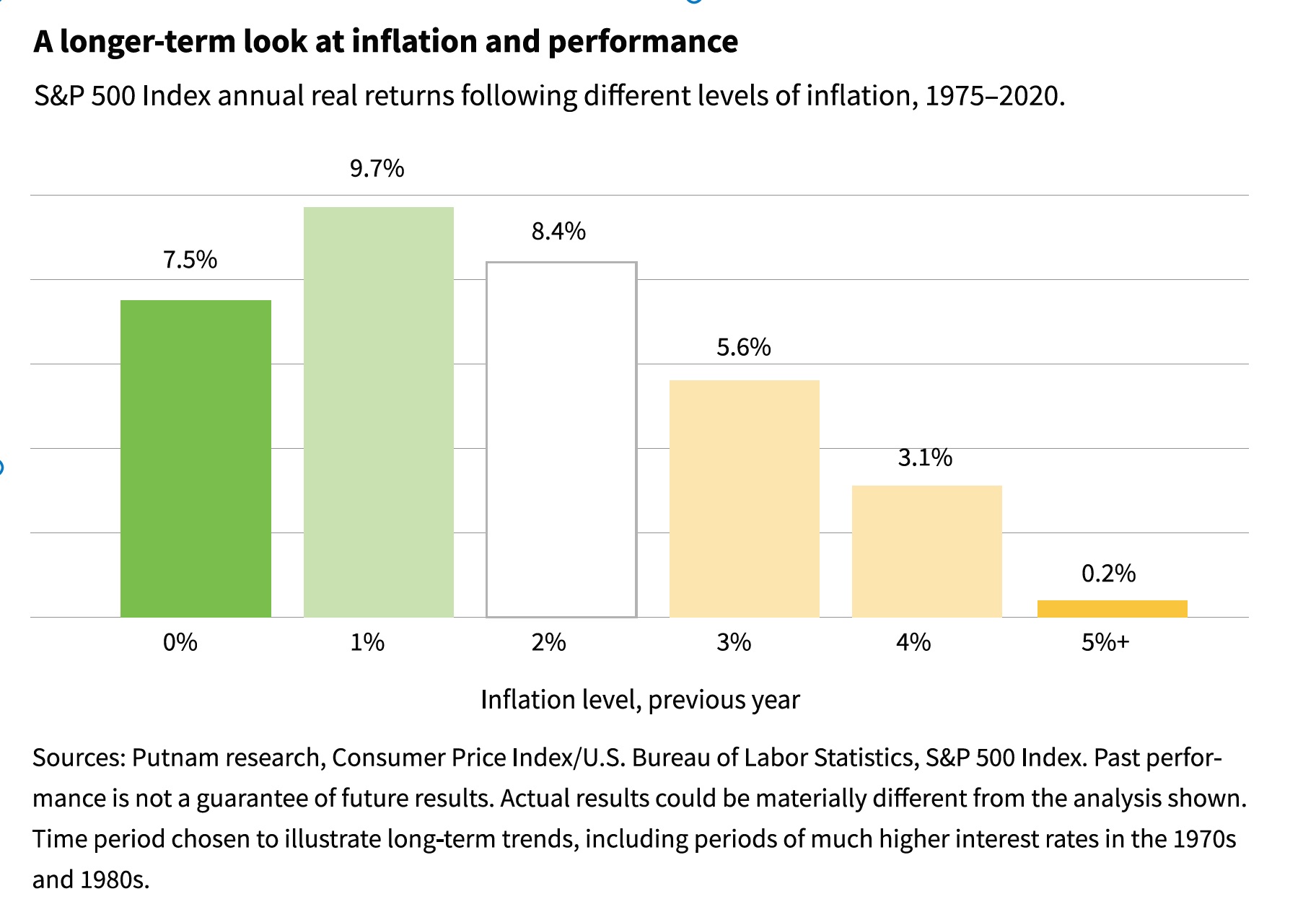

The inflation “sweet spot” for stock performance

DON: We Looked at inflation rates for one-year periods from 1974 to 2020. We then analyzed the equity market’s real return — the market return adjusted for inflation — for the following year. We found:

- Zero to 2% inflation was best for equity performance in the following year.

- Higher levels of inflation resulted in weaker returns.

- Inflation sustained above 3% has historically been a drag on equity returns.

Some industries thrive with higher inflation

DON: Our analysis showed how changing inflation levels affect different industries. Some businesses clearly fare better in inflationary environments. They include companies whose products and services remain in demand regardless of macroeconomic conditions. Although input costs may rise, these businesses still perform well because they are able to pass the cost increases on to consumers. Also, there are not ready replacements for their goods, most of which are necessities.

For example, when inflation was higher, average returns for telecommunications services, food retailing, and energy stocks were more than 10% higher, while returns for software and services stocks were more than 30% lower.

Don’t overlook inflation risk

SHEP: Our research suggests that equity markets are likely to hold up well despite rising inflation, especially because we are emerging from a period of historically low interest rates and inflation. However, rising inflation should not be disregarded as a risk for equity investors. What’s different today is that the composition of the S&P 500 is skewed more toward growing, asset-light, and high-quality companies — the stocks of which may be more vulnerable to higher inflation-led interest rates. Historically, when inflation accelerates sustainably beyond 3%, it has dampened real equity returns.

Goodbye to Goldilocks

For many years, the equity market has benefited from low inflation expectations and no deflation, which is a near-perfect Goldilocks scenario. As we move out of this range, we should see a shift in market leadership. We could see disruption in the form of sharp sector rotations as so much of equity ownership today is skewed toward growth. In our view, high-growth stocks would be particularly vulnerable, as their elevated multiples have the farthest to compress. Until recently, investors have shunned stocks in cyclically sensitive sectors — those that tend to do well with higher inflation.

The strategy for rising inflation

We believe active portfolio management is key to addressing this challenge. The ability to monitor conditions, shift industry weights, and select stocks that can benefit from rising inflation will be critical in navigating a changing environment in the months ahead.

This material is prepared for use by TEXPERS and is provided for limited purposes. By receiving and reviewing this material, the recipient acknowledges the following: This material is a general communication being provided for informational and educational purposes only. It is not designed to be a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The material was not prepared, and is not intended, to address the needs, circumstances and objectives of any specific institution, plan, or individual(s). Putnam is not providing advice in a fiduciary capacity under applicable law in providing this material, which should not be viewed as impartial, because it is provided as part of the general marketing and advertising activities of Putnam, which earns fees when clients select its products and services. Unless otherwise noted, Putnam is the source of all data. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the material. Predictions, opinions, and other information contained in this material are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks and uncertainties. Actual results could differ materially from those anticipated. Past performance is no guarantee of future results. This material or any portion hereof may not be reprinted, sold, or redistributed in whole or in part without the express written consent of Putnam Investments. The information provided relates to Putnam Investments and its affiliates, which include The Putnam Advisory Company, LLC. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of TEXPERS. Views are subject to change over time. Follow TEXPERS on Facebook, Twitter, and LinkedIn for the latest news about the public pension industry in Texas.