|

|

With European bank valuations at a 33-year low, let's examine why this may be this best time to invest with the right strategy.

|

|

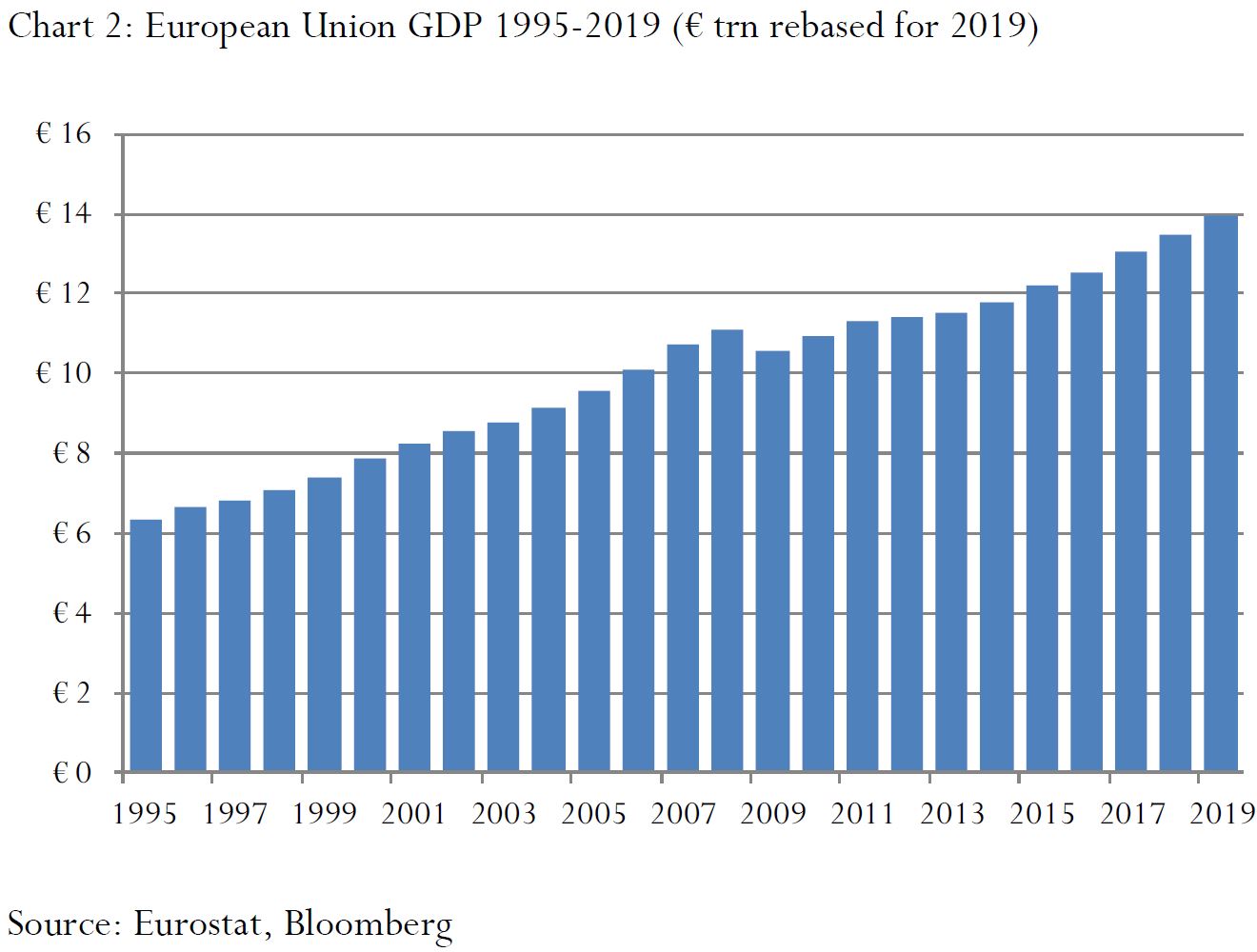

33 years is a long time…The STOXX Europe 600 Banks Index, the most used benchmark for European banks valuations, closed at a dismally low level of 82 on 24 April 2020, a level not seen even during the depths of the global financial crisis (GFC) of 2008. The last time it saw this level was in the fall of 1987. This is truly astonishing considering that the size of the European economy has more than doubled in the meantime (see Chart 2), and banks’ balance sheets have grown at an even faster pace. |

|

|

As Chart 3 illustrates, European and US banks valuations were comparable until the GFC. While the indices began 1992 around the level of 100, the Dow Jones US total market banks index has recovered post-GFC to reach those levels again prior to the recent sell-off. The same cannot be said of the STOXX 600 Europe, which has struggled since the GFC, rarely reaching 200. On 24 April 2020, the US banks index closed at 313, compared to Europe’s 82. |

|

|

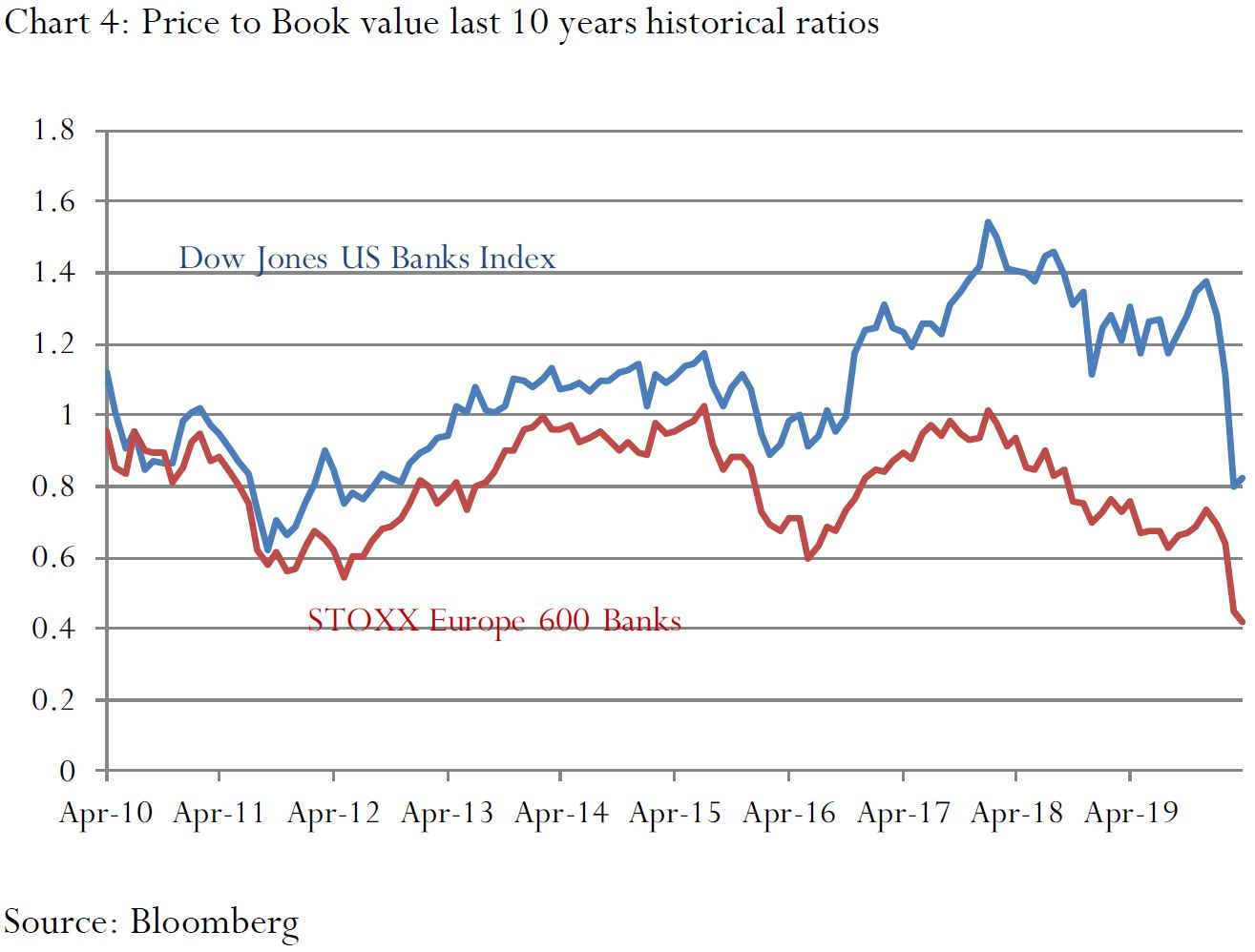

Similar trends can be observed when looking at valuation metrics such as Price-to-Book Value, with European banks |

|

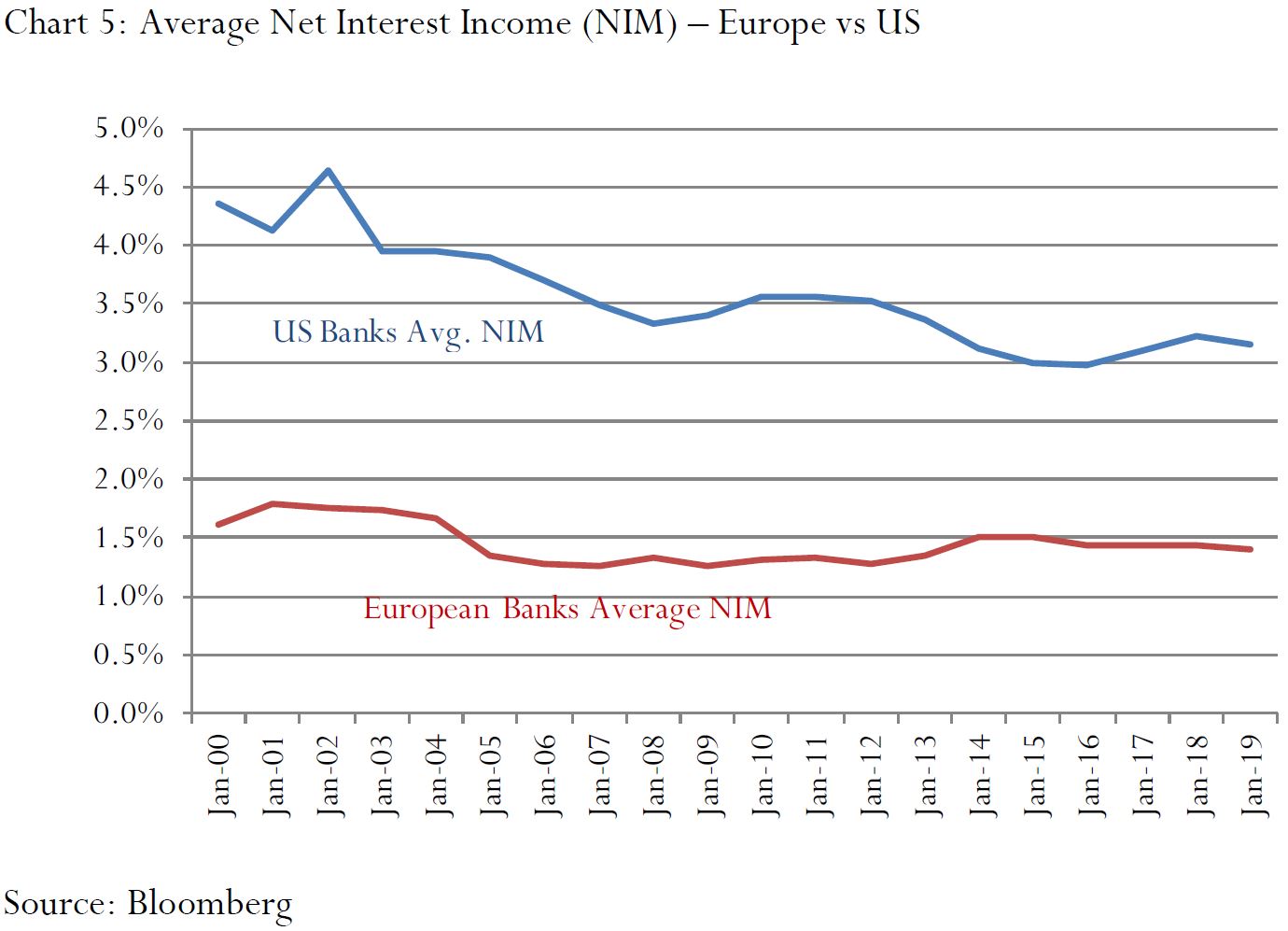

2010s - the “Lost Decade” for European banks?It may be unfair to describe the 2010-2020 as the Lost Decade for European banks, as doing so ignores the progress that has been achieved during the decade. Objectively, European banks capital ratios and the gross amount of primary loss absorbing capital are multiples of what they were prior to the GFC. Asset quality has also substantially improved and in some cases exceeded levels prior to the GFC, with other fundamental metrics also improving. But profitability has suffered even before the onset of the COVID-19 crisis. As a result, the biggest beneficiaries of the last ten years have been bank credit investors, and this to some extent came at the expense of equity investors. Why? Simply put, higher capital means lower return on equity (ROE), everything else held equal. We focus here on themes that have broad impact on European banks and, where relevant, compare them to trends in the US. (1) Difference in product mix. In general, European banks have more low-margin assets on their balance sheets as compared to their US counterparts (see Chart 5). In Europe, mortgages comprise a significant portion of loan books. They are generally considered to be safe assets and have a low risk weighting. But this also translates into a lower margin versus unsecured lending. |

|

|

(2) European banks balance sheet cleanup was slower than the US, post-GFC. Many undercapitalized banks would have had to take unabsorbable asset write-downs to suitable levels for a third-party sale, and hence clean their balance sheet for new loans. The ECB then expanded the type of securities it would accept as collateral (e.g. so-called “retained covered bonds”), so even weaker banks were able to access liquidity. Banks generally will not fail by exhausting capital – rather the problem is capital deficit leading to a liquidity crunch. But as the actions of the ECB alleviated the liquidity threat, they also blunted the urgency to fix the problems, which has contributed to the lackluster 2010s EU economic growth. (3) Management failure – investment banking. The GFC took place during the same period as the Basel Committee for Banking Supervision (BCBS) began implementing Basel II. This made some of the most profitable areas much less profitable or uneconomical altogether due to significant increases in capital requirements. These major changes were often treated by management teams as being cyclical rather than secular in nature. Furthermore, scale has become much more important to maintain profitability, a trend that has also hurt European banks’ investment banking operations. (4) Management failure – commercial and retail banking. European banks in general have been underperformers in cost management. There are exceptions. Scandinavian or Dutch banks that have cut their retail branch footprint by over 60-70% in the last ten years, but the vast majority have been complacent. The cost / income ratio of US banks it is on average 10% below that of European banks. (5) Lack of consolidation – The need for consolidation is something most regulators and policymakers in Europe agree on in principle, but less so in practice. The aborted merger of Commerzbank and Deutsche Bank in the spring of 2019 is just one example. There are still far too many regulatory and legal hurdles for consolidation to scale, but this may change as a result of the challenges brought on by the COVID-19 crisis. (6) Growth story, yield story or no story – The latest turn for the worse in European banks equity valuation came due to regulator’s advice to suspend dividend payments for the duration of the COVID-19 crisis. These dividend suspensions were accompanied by temporary loosening of countercyclical capital buffers and provisioning rules to encourage further lending. Unfortunately, most large European banks have built their entire investment thesis on high dividend ratios and attractive yields. Healthy share prices require a growth story or a dividend story, and alas, for most large European banks, presenting a growth story in a lackluster macro-economic environment, even prior to the COVID-19 crisis, was a non-starter, and now the dividend yield story thesis has also been invalidated. European banks – value trap or opportunity?There was nothing inevitable about where European banks find themselves today – it happened as a result of decisions taken by individuals. That’s the bad news. The good news is that most of the causes of underperformance are fixable given the right mix of expertise, people, capital and technology. It is also worth noting here that successful investors in the European banks space need to take view during this period of uncertainty, as once its direction of travel is clear, 90% of the value will likely have been priced in. |

|

| Financial Services Capital is an Associate member of TEXPERS. This Article is not an offer to sell, or an invitation for an offer to acquire, an interest in any investment, nor is it an invitation to apply to participate in any investment. This Article is not an offering or placement of interests in any investment in any jurisdiction, and should not be construed as such. Follow TEXPERS on Facebook, Twitter and LinkedIn as well as visit our website for the latest news about Texas' public pension industry. |

Jun

29

Share this post: