A Historical Analysis of Inflation's Impact on Real Estate

|

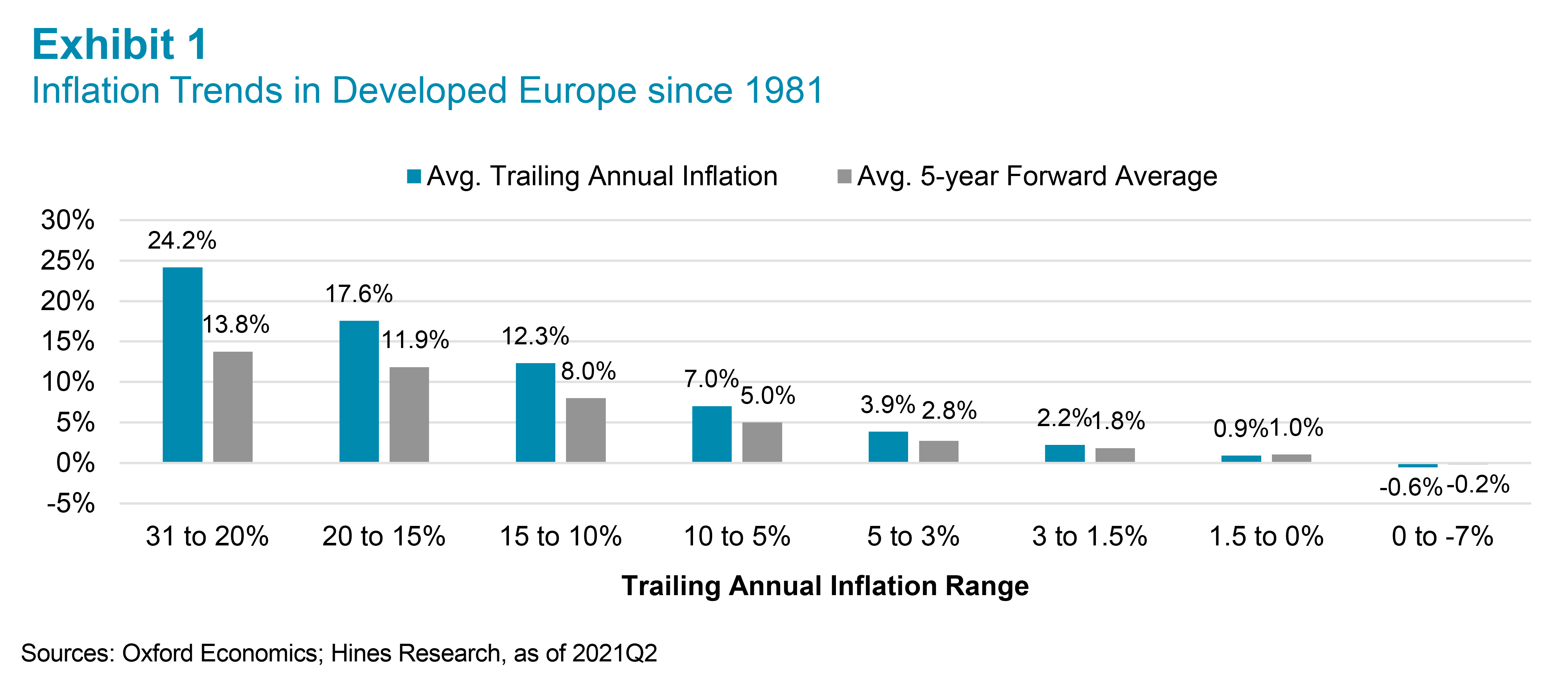

Temporary bouts of inflation have arisen in the last two decades, prompting questions that result in lengthy webinars and white papers on the matter as those bouts materialize. On the surface, concerns about inflation appear valid. After all, the notion that higher inflation leads to higher borrowing costs, therefore increasing cap rates and applying downward pressure on valuations, is a simple concept to latch onto and cause worry. In addition, the massive injections of liquidity that governments and central banks have deposited into the global economy over the past dozen years add support for concerns of runaway inflation. However, the relationship between inflation, interest rates and commercial real estate cap rates is more complex than what simple framework suggests, with growth expectations playing a large role in the interconnection of those metrics. When cap rate spreads over other yielding assets, such as the currently wide sovereign bond yields, and rent growth expectations are good, value growth over the following 2-5 years tends to be quite good, even with an increase in inflation and interest rates. I would characterize current growth expectations as solid, but certainly not astounding. However, that is a generalization, as conditions vary dramatically across markets. Much of my past work on the subject matter has focused on these relationships. Rather than rehashing that past work, this paper will look at past periods of varying inflation and examine the impact that those inflationary environments had on the performance of real estate metrics over the following five years. Past Bouts of Inflation Have Proven to Be Highly TransitoryIn nearly all geographies, extreme inflation levels tended to be quite transitory, whether unusually low or high. Exhibit 1 utilizes data set across 14 developed European economies[1] and the U.K. over the past 40 years. Conclusions were similar when testing this across other economies in Asia-Pacific, North America, and developing economies in central and eastern Europe. |

|

|

|

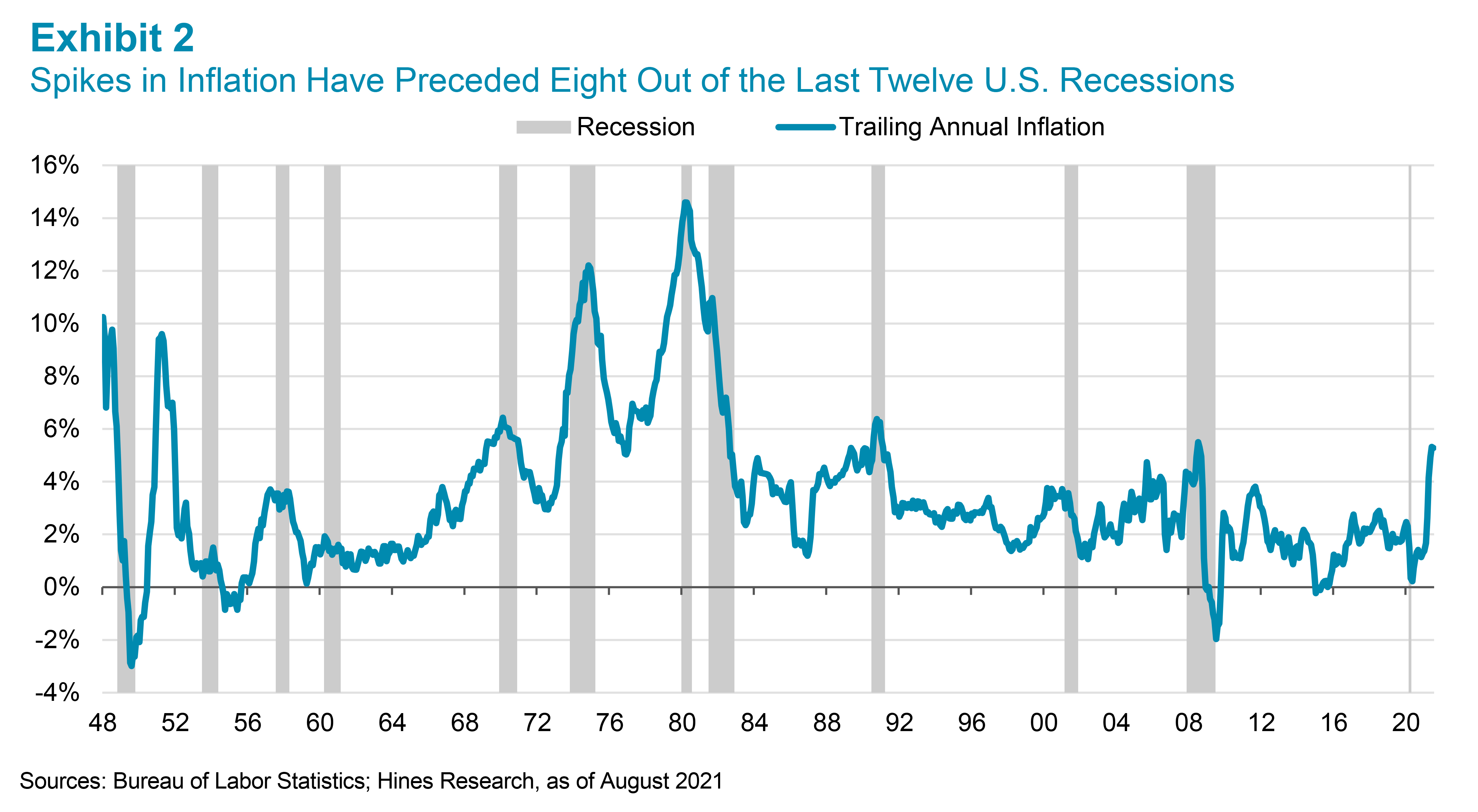

Exhibit 1 highlights trailing annual inflation across the 14 economies as illustrated by the blue bars versus average future inflation over the following five years as represented by the gray bars. In periods when trailing inflation is in the 3-5% range, inflation has averaged approximately 110 basis points lower over the following five years. Inflation is currently at 3% in the Eurozone and 3.2% in the U.K. In the early 1980s, when inflation was undoubtedly high in many countries–Italy, Portugal, Norway, etc., it fell dramatically over the following five years. Following periods when inflation was unusually low, it has tended to increase, although this phenomenon is more muted in developed Europe than it is in many geographies. As mentioned, this occurrence holds true across a diverse array of economies, whether developed or developing, and even in countries like Brazil with reputations for inflation spikes. In the latter, anytime inflation has risen above 9%, since the institution of Brazil’s modern currency in July 1994, it has fallen 100% of the time over the following two years. And not just by a little, but by about two-thirds on average (i.e., 9% falling to 3% within two years, 12% falling to 4%, etc.). Why is this? Economists worry about high inflation that leads to higher expectations of inflation and therefore becoming self-fulfilling, but the empirical evidence of that occurring is weak, and inflation has tended to be more dynamic than static for many reasons. Indeed, the current ramp-up in production, business investment, and supply chain reconfiguration that is in process should close the supply/demand imbalances that drive prices higher across many industries and countries over the next couple of years. This scenario will be even truer as the pent-up pandemic lockdown demand is ultimately spent up. By way of one example, consider that the U.S. created a grand total of 38,000 new households from July 1, 2019, through July 1, 2020, per the U.S. Census Bureau. Like many statistics during the pandemic, 38,000 is an incredibly low number, as the U.S. creates approximately one million new households in a typical year. Therefore, as the economy reopened and people began to form households once again, a two-year wave of housing demand was unleashed in a relatively short period of time. This resulted in frenzied demand for all kinds of housing, whether it was for rent or for sale. At some point, that pent-up demand will be satisfied, and more ordinary levels of demand will meet with rising levels of supply to create more sustainable levels of rental and price inflation (i.e., lower). While housing demand and supply are close to our real estate hearts, this experience is likely playing out in a wide swath of industries and markets. In the U.S., for example, total business investment over the past four quarters has been running at 2.4x its pre-pandemic averages from 2018-19, and much of that investment is surely tied to increasing production capacity and reconfiguring supply chains to meet outsized demand. Inflation’s Impact on Future Real Estate PerformanceSince the U.S. has the longest duration and most reliable commercial real estate data, we will utilize the U.S. commercial real estate data for this analysis. While the assumption that the U.S.’s results are applicable to all economies may be a bit of a stretch, the benefits of the larger and longer data set are significant. So, while the U.S. experience may not be 100% applicable to all real estate markets, it will at least provide some baseline guidance as to the impact that higher levels of inflation have had on real estate fundamentals and capital markets in the years that follow. In a very simple analysis comparing inflation levels with real estate returns, higher levels of inflation have coincided with higher returns since 1978, both nominal as well as real. However, those returns have been concurrent with inflation rather than following periods of high inflation. And because high inflation has tended to be transitory as discussed earlier, what we want to know is how that higher inflation has impacted future performance rather than concurrent performance. One of the more disconcerting findings that I didn’t fully appreciate as I undertook this research is that bouts of inflation have preceded eight out of the last twelve U.S. recessions, as shown in Exhibit 2. Ultimately, while the cause and nature of recessions can be quite different, recessions are primarily about the correction of economic imbalances, and those periods of high inflation likely reflected some of the imbalances that eventually caused the recessions that followed. Of course, higher inflation can also force central banks’ hands, and rising interest rates can also stifle economic output, thereby leading to recessions. |

|

|

|

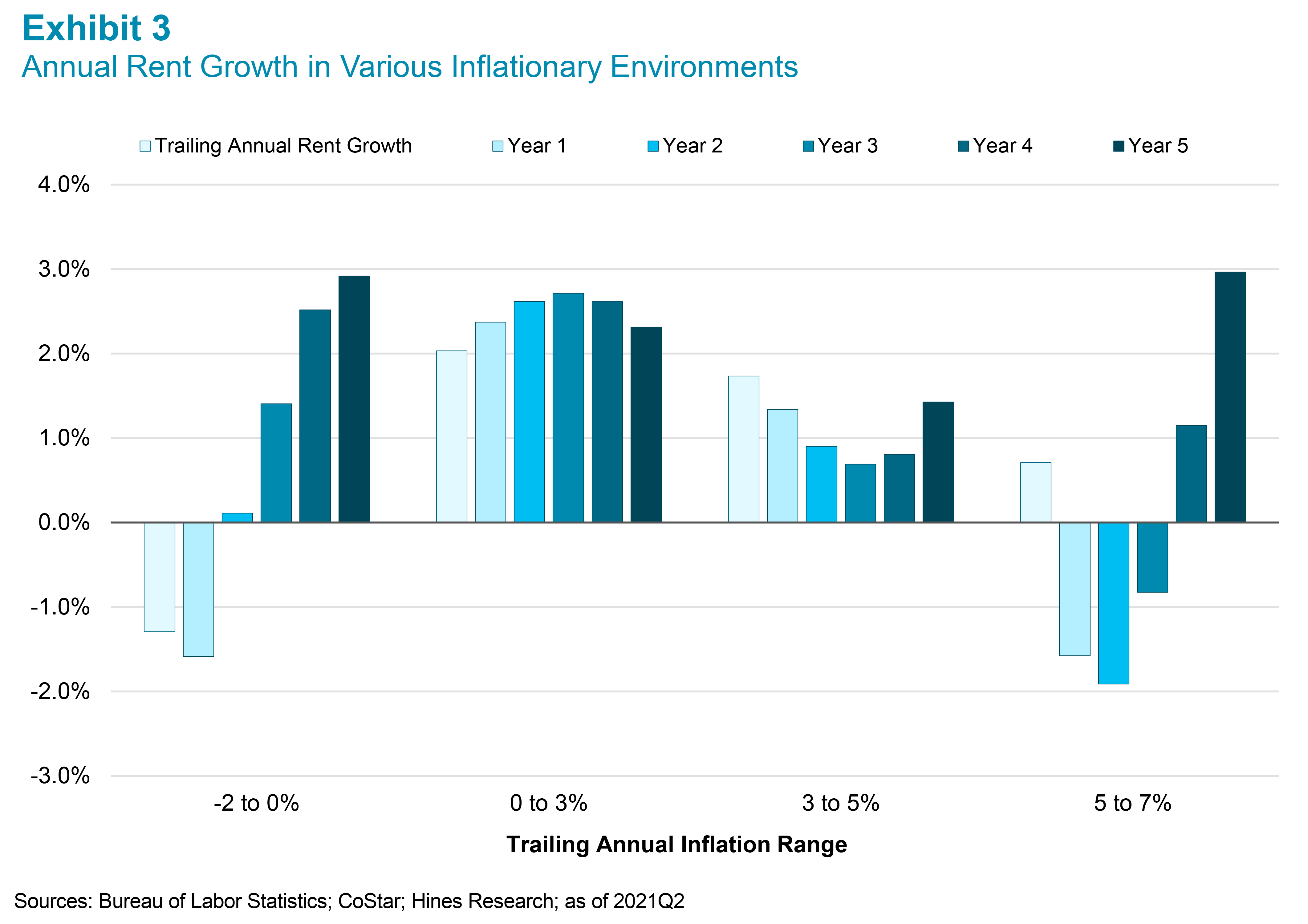

While I do not put a lot of stock in economic forecasts, I do review forecasts and there are few, if any, prognosticators that call for a double-dip recession in 2022. I recognize that recessions have followed periods of inflation since the early 1980s. In addition, the resultant historical impact on commercial real estate markets may be less informative if the economy continues to recover as most expect. However, if delta and/or supply bottlenecks continue to harm the economy, we can appropriately stress test our underwriting and prepare for potential headwinds. In Exhibit 3, we illustrate the average pattern of annual rent growth on a trailing annual basis and over the five years following various inflationary environments. Low and steady inflation in the 0-3% range has generated both the steadiest and strongest rent growth over the following five years. From this, one can see an average of 5-year forward CAGR of 2.6%. When consumer prices have fallen in the preceding year or have risen by more than 5%, rent growth has tended to be much more dynamic, with a period of annual declines giving way to recovery in the outer years. In a moderately high inflationary environment of 3-5% price gains, trailing annual average growth of 1.7% has eased with a 1% CAGR average over the following five years. However, the market has avoided the kind of losses experienced in very high or low inflationary atmospheres. Within the 3-5% range, apartments have historically outperformed over the following five years, with a rent growth CAGR of 1.8% followed by industrial at 1%, office at 0.8%, and retail at just 0.5%. |

|

|

|

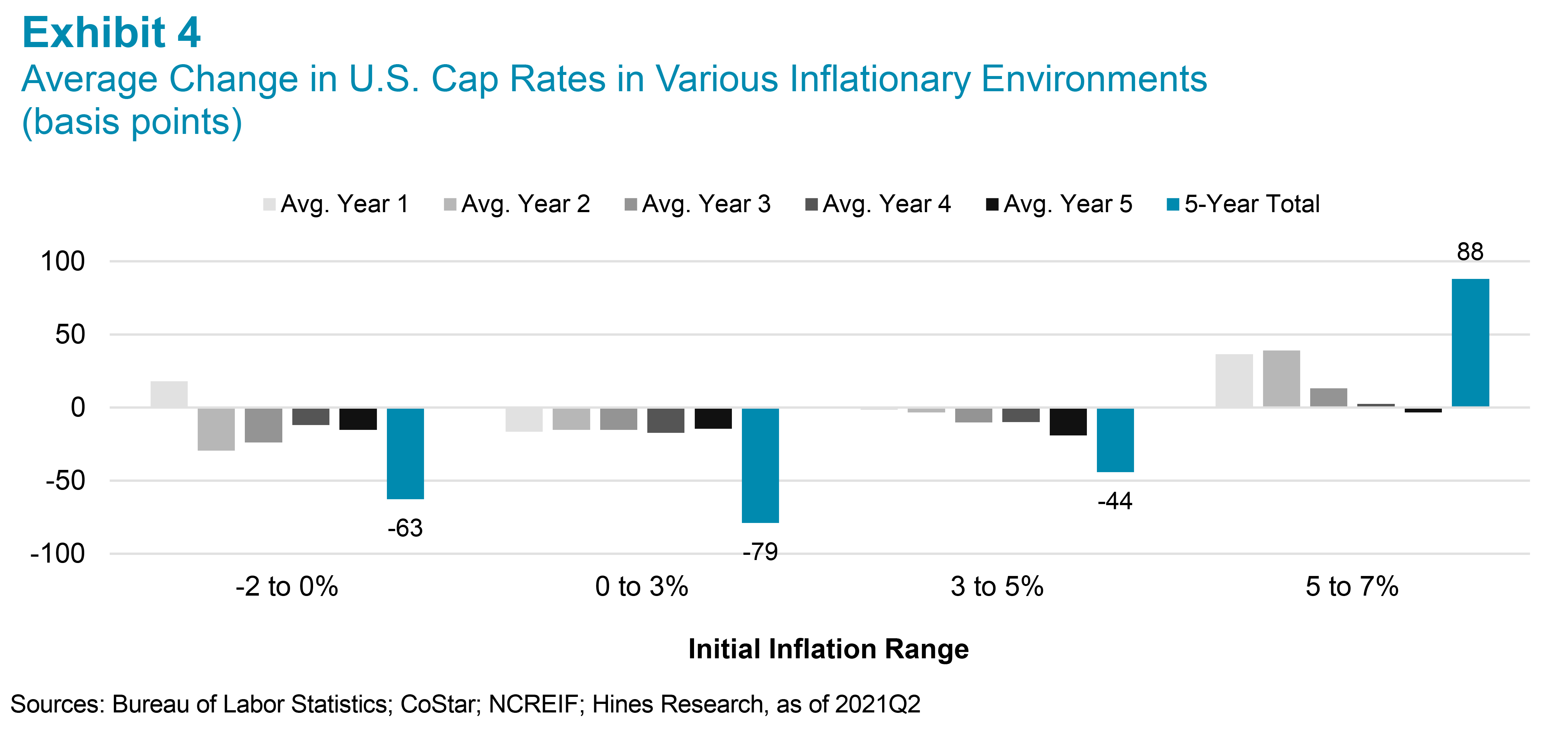

Other than a few brief periods, falling interest and cap rates have tended to dominate the real estate data over the past 30 years. That said, we can look at the relative decline in cap rates following various inflationary environments in Exhibit 4. Once again, low, stable inflation is preferred as it has tended to coincide with the steadiest and most significant cap rate compression over the following five years. While average cap rates have risen in year one when inflation has been negative, likely due to weak aggregate demand in a recessed economy, the cap rates have tended to decline over the following four years. This scenario generated an average of 63 basis points of compression over the entire five-year period. Following moderately high inflation in the 3-5% range, cap rates have also fallen, though by just 44 basis points on average. Only when inflation has exceeded 5% has the market experienced cap rate expansion over the following five years, keeping in mind, of course, the caveat that recessions have followed inflation spikes of 5% or more since the onset of modern real estate performance data. |

|

|

|

Conclusions We could continue this analysis further and have in prior papers on the subject matter, but in the spirit of brevity, here are some key takeaways:

|

| Sources:[1] Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Netherlands, Norway, Portugal, Spain, Sweden, and the U.K. About the Author and Hines Proprietary Research:

The Hines Proprietary Research team includes Michael Hudgins, Ryan McCullough, Farhaz Miah, Michael Spellane and Erik Thomas. DisclaimerPast performance is no guarantee of future results. Investing involves risks, including possible loss of principal. The opinions presented herein cannot be viewed as an indicator of future performance. Confidential Information This document is intended only for the recipient to whom it has been furnished by Hines. The reproduction of this document in whole or in part is prohibited. You are not permitted to make this document, or the information contained herein and/or the information provided to you, available to any third parties. Preliminary Selective Information This document is being provided to you on a confidential basis for the sole purpose of providing you with initial and general information at your own responsibility. This document is not suitable to inform you of the legal and factual circumstances necessary to make an informed judgment about any prospective investment. Prospective investors are requested to inform themselves comprehensively and, in particular, to verify the contractual documentation that will be provided in the future. Not an Offer This document does not constitute an offer to acquire or subscribe for securities, units or other participation rights. The distribution of this document is reserved to institutional investors and may be restricted in certain jurisdictions. It is the responsibility of the recipient of this document to comply with all relevant laws and regulations. Third Party Information This material contains information in the form of charts, graphs and/or statements that we indicate were obtained by us from published sources or provided to us by independent third parties, some of whom we pay fees for such information. We consider such sources to be reliable. It is possible that data and assumptions underlying such third-party information may have changed materially since the date referenced. You should not rely on such third‑party information as predictions of future results. None of Hines Interests Limited Partnership (“Hines”), its affiliates or any third-party source undertakes to update any such information contained herein. Further, none of Hines, its affiliates or any third-party source purports that such information is comprehensive, and while it is believed to be accurate, it is not guaranteed to be free from error, omission or misstatement. Hines and its affiliates have not undertaken any independent verification of such information. Finally, you should not construe such third‑party information as investment, tax, accounting or legal advice. Forward Looking Statements This material contains projected results, forecasts, estimates, targets and other “forward-looking statements” concerning proposed and existing investment funds and other vehicles. Due to the numerous risks and uncertainties inherent in real estate investments, actual events or results or the actual performance of any of the funds or investment vehicles described may differ materially from those reflected or contemplated in such forward-looking statements. Accordingly, forward‑looking statements cannot be viewed as statements of fact. The projections presented are illustrations of the types of results that could be achieved in the given circumstances if the assumptions underlying them are met but cannot be relied on as accurate predictions of the actual performance of any existing or proposed investment vehicle. Disclaimer The statements in this document are based on information that we consider to be reliable. This document does not, however, purport to be comprehensive or free from error, omission or misstatement. We reserve the right to alter any opinion or evaluation expressed herein without notice. Statements presented concerning investment opportunities may not be applicable to particular investors. Liability for all statements and information contained in this document is, to the extent permissible by law, excluded. |

| Disclaimer: Hines is an Associate member of TEXPERS. The views and opinions contained herein are those of the author, and do not necessarily represent the views of Hines nor TEXPERS. These views are subject to change. Follow TEXPERS on Facebook, Twitter and LinkedIn as well as visit our website for the latest news about Texas' public pension industry. |

Joshua Scoville, is Senior Managing Director – Research, and reports to Hines’ Chief Investment Officer and works closely with the firm’s Chief Risk Officer and Strategy Group. Scoville and his team are responsible for constructing the Hines macroeconomic view and outlook for commercial real estate market fundamentals and pricing; assisting with the development of investment strategies for the firm’s investment programs; working closely with the local and fund management teams, clients and partners; and supporting U.S. regional and international country heads in identifying market/submarket opportunities and risks. The views of the local and fund management teams on the latest market developments are exchanged regularly via biweekly conference calls and quarterly market updates and are essential for reviewing investment strategies and fund portfolio allocations.

Joshua Scoville, is Senior Managing Director – Research, and reports to Hines’ Chief Investment Officer and works closely with the firm’s Chief Risk Officer and Strategy Group. Scoville and his team are responsible for constructing the Hines macroeconomic view and outlook for commercial real estate market fundamentals and pricing; assisting with the development of investment strategies for the firm’s investment programs; working closely with the local and fund management teams, clients and partners; and supporting U.S. regional and international country heads in identifying market/submarket opportunities and risks. The views of the local and fund management teams on the latest market developments are exchanged regularly via biweekly conference calls and quarterly market updates and are essential for reviewing investment strategies and fund portfolio allocations.