|

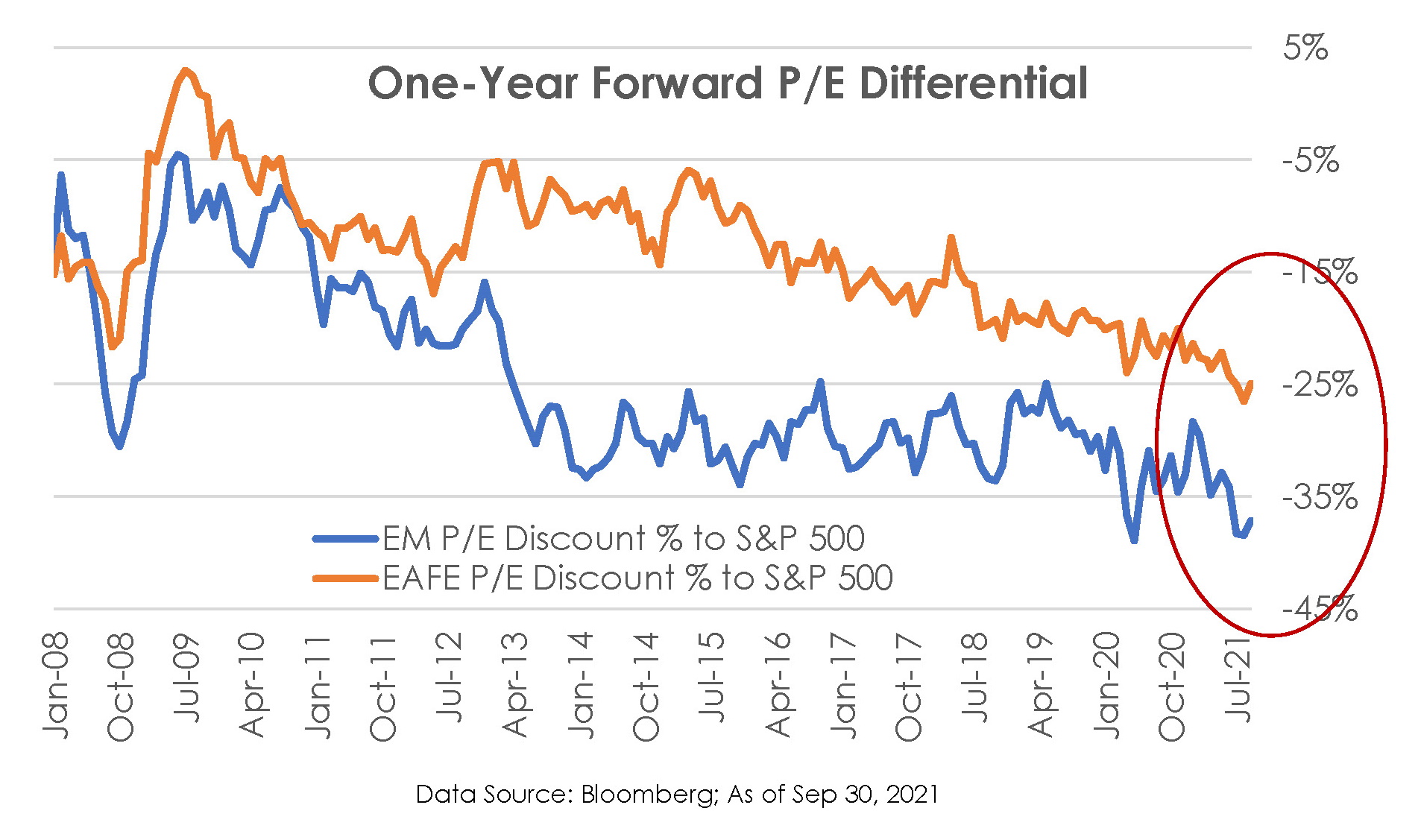

As U.S. equities outperformed over the last decade, helped by superior earnings growth and innovation, relative valuations of international stocks have fallen steadily. In fact, the valuation differential between U.S. and international equities is at its widest since the 2008 financial crisis. With improved operating margins, beneficial structural trends, the likely capex revival, and fiscal spending, are international stocks positioned to outperform? We believe so. Lowest Valuations since 2008 Based on expected earnings for next year, developed international stocks, represented by the MSCI EAFE Index, are now 25% less expensive than the S&P 500. The valuation discount for emerging markets, using the MSCI EM Index, is even wider at over 35%. |

|

|

|

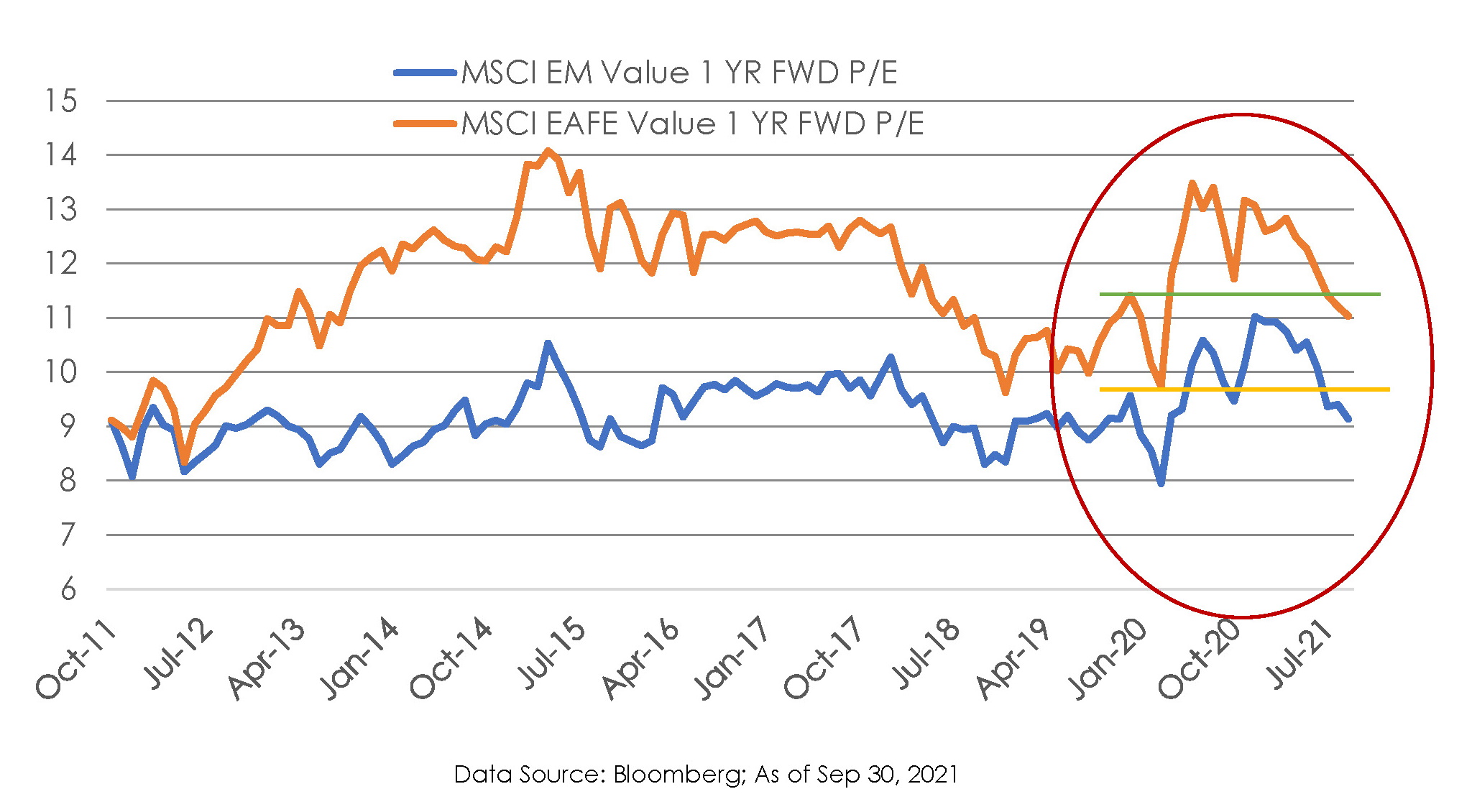

International Value Stocks Are Now Cheaper Than Pre-Pandemic It is a common refrain that the strong market recovery from the lows of early 2020 has led to apparent excessive equity valuations everywhere. Investors who fret about expensive stocks in the U.S. and elsewhere seem to have missed international value stocks that are now cheaper than pre-pandemic levels, based on one year-forward earnings. Value stocks in emerging markets are now trading at less than 10 times their forecast earnings for the coming year. |

|

|

|

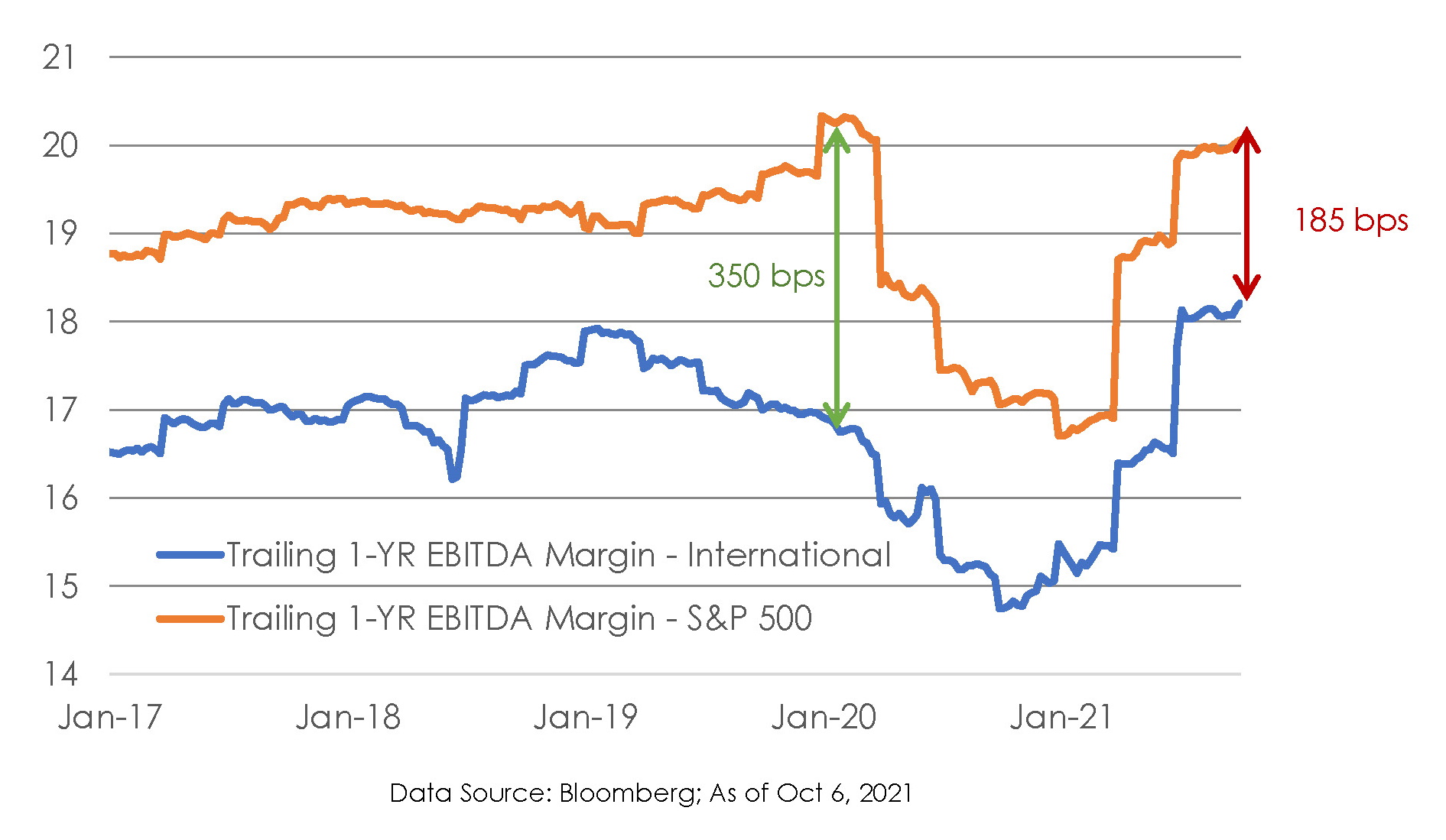

Margin Improvements Have Gone Unnoticed Much of the U.S. equity outperformance over the last decade was underpinned by fatter margins and stronger earnings growth. American companies continue to enjoy higher profit margins, on average. Yet, investors seem to have so far ignored the meaningful improvement in operating margins of international companies. At the beginning of 2020, before the pandemic hit, trailing EBITDA margins of S&P 500 companies were about 350 bps better than international companies, as represented by the MSCI ACWI ex U.S. Index). American companies still have better margins, but the gap has nearly halved to 185 bps now. |

|

|

|

Favorable Trends Could Help Sustain Earnings Several large non-U.S. companies are likely to see a multi-year boost to their revenues and earnings from some of the major structural changes happening globally. Be it from digitization of everyday products and services that are driving robust semiconductor demand or the dramatic increase in investments related to renewable energy and climate change, international companies are positioned to benefit as much as their U.S. peers, if not more. After more than a decade of underinvestment, even conventional industrial manufacturers and miners are likely to step up capital investments in the coming years. The established capital goods manufacturers in Europe and Japan should get a revenue lift when that happens. Finally, unlike in the U.S. where fiscal spending to recover from the pandemic was heavily front-loaded, governments in Europe and Japan are likely to sustain spending next year as well. Long-term Investors Should Look Beyond Headlines Its no surprise that alarming news headlines have kept many investors cautious about international equities. The Chinese government seems determined to rein in some of the country’s best-known companies, while at the same time trying to limit systemic risks from overleveraged property developers on the verge of default. Supply chains remain disrupted across the globe, pushing up costs and reducing sales volumes. In addition, there are the still lingering U.S.-China tensions and policy uncertainties in Germany and Japan due to recent leadership changes. Yet the probability of any of these developments escalating to trigger a deep market decline appears low. The Chinese government so far seems to be in control of its efforts to reduce excessive leverage, household expenses, and the concentration of market power. Global supply chain dislocations should clear eventually, though it is taking much longer than expected. The U.S. and China continue to diplomatically engage each other, with a possible presidential summit later this year. As these geopolitical and regulatory clouds clear, we believe patient long-term investors who recognize the improved earnings growth potential of relatively inexpensive international equities are poised to be rewarded. |

About the Author: Rex Mathew is Senior Vice President and Portfolio Manager at Thomas White International, a minority-owned boutique asset management firm based in Chicago, Illinois. He covers companies based in Europe, Asia-Pacific Including Japan, Canada, emerging markets in Asia outside China, and Latin America for the firm's international and emerging markets portfolios. He also leads the global markets, economy, and industry analysis efforts that supports the firm's investment research as well as development of written content that highlight the firm's investment and market insights. Disclaimer:Thomas White International is an Associate member of TEXPERS. This article is for informational purposes only, is not investment advice, and should not be considered a recommendation to buy or sell any security or to invest in any particular market or country. Actual future results or occurrences may differ significantly from those anticipated. Follow TEXPERS on Facebook, Twitter and LinkedIn as well as visit our website for the latest news about Texas' public pension industry. Rex Mathew is Senior Vice President and Portfolio Manager at Thomas White International, a minority-owned boutique asset management firm based in Chicago, Illinois. He covers companies based in Europe, Asia-Pacific Including Japan, Canada, emerging markets in Asia outside China, and Latin America for the firm's international and emerging markets portfolios. He also leads the global markets, economy, and industry analysis efforts that supports the firm's investment research as well as development of written content that highlight the firm's investment and market insights. Disclaimer:Thomas White International is an Associate member of TEXPERS. This article is for informational purposes only, is not investment advice, and should not be considered a recommendation to buy or sell any security or to invest in any particular market or country. Actual future results or occurrences may differ significantly from those anticipated. Follow TEXPERS on Facebook, Twitter and LinkedIn as well as visit our website for the latest news about Texas' public pension industry. |