Middle-market Stocks Can Help Portfolios Cope With Volatility

Equity markets were jolted in January amid growing concerns about macroeconomic threats. For investors seeking more stable equity allocations, stocks “in the middle,” with high-quality features and reasonable valuations, can help portfolios cope with volatility.

With inflation rising, fears that policymakers could tip economies into recession have eroded enthusiasm for stocks after three strong years. Hypergrowth names at the most expensive extreme of the US market were hit hardest. We believe these trends reinforce the need for defensive equity strategies to help reduce risk in a downturn and capture recovery potential.

In good times and bad, predicting macroeconomic and policy trends isn’t a prudent strategy for equity investors, in our view. Instead, investors can seek to build a macro-resilient portfolio by investing in companies with features that are likely to withstand the key risks to equity markets. Today, those risks are interest rates/inflation, valuation and a decelerating growth outlook.

Position for Heightened Inflation

Inflation and interest rates are the biggest source of uncertainty today. While the US Federal Reserve and Bank of England have signaled plans for aggressive rate hikes, the European Central Bank has taken a more moderate stance. Market volatility is being fueled by a tension between concerns about monetary policy and signs of solid corporate earnings.

In this environment, equity investors must distinguish between businesses that are more likely to do well in an inflationary environment and those more vulnerable to higher prices. Defensive portfolios should also aim to identify companies with fundamentals that are more likely to hold firm if efforts to combat inflation trigger a worse-than-expected economic slowdown.

High-quality companies are always an important component of a lower volatility equity allocation, in our view. But given the inflation risks, pricing power is an especially important quality feature today. Companies with pricing power will find it easier to maintain margins as inflation rises. Those with significant intangible assets, such as proprietary data, R&D and human capital, are also likely to enjoy pricing power. Even in technology, a sector that isn’t usually seen as defensive, some companies have more pricing power today than in the past.

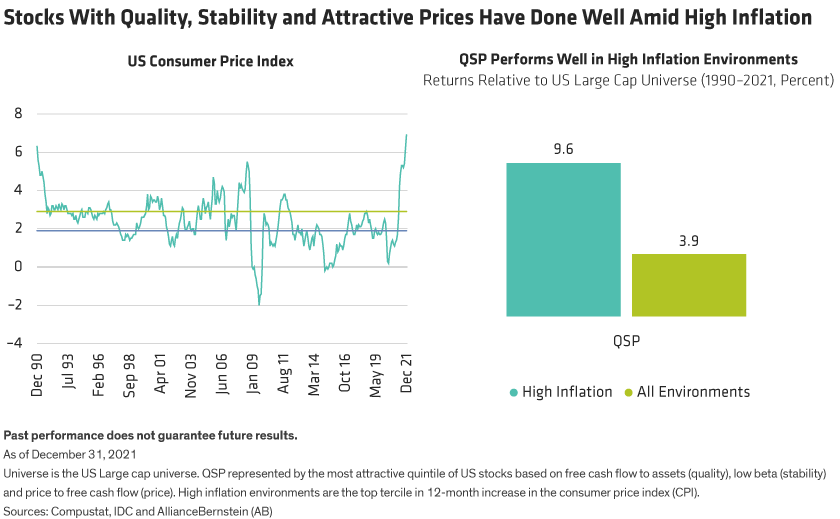

Quality alone isn’t enough. We believe quality companies with relatively stable stock prices and attractive valuations are the best way to reduce volatility in an equity portfolio. These characteristics tend to perform well in inflationary environments, too. Our research suggests that the most attractive quintile of US companies based on free cash flow to assets (quality), low beta (stability) and price to free cash flow (price) delivered an annualized return of 9.6% in inflationary environments (Display). That’s more than double the performance of this group of stocks in all environments because high inflation has historically been followed by economic slowdowns and recession.

Certain types of defensive equities, such as low-beta stocks, have underperformed in the past when interest rates rose. However, these risks can be managed by active investors who reduce exposure to sectors and companies that are more vulnerable to inflation and interest-rate risk.

Valuations and Volatility

Recent market volatility refocused attention on valuations. In 2021, rising valuations were driven primarily by strong earnings growth amid the rebound from the pandemic-induced collapse. With earnings growth forecast to fall back to more normal levels in 2022, concerns about valuations are understandable.

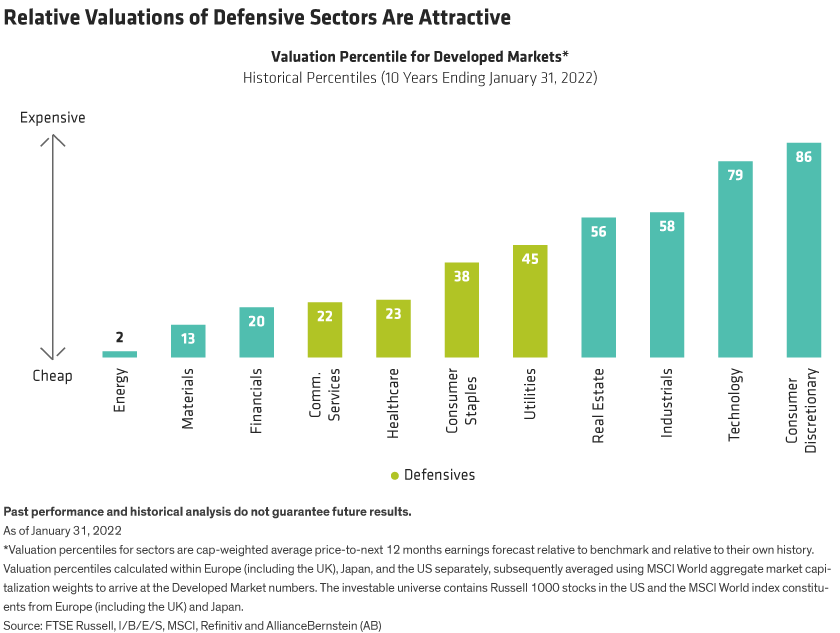

But valuations across sectors and within industries are diverse—particularly in defensive stocks. In consumer staples and health care, for example, equities are much cheaper than they’ve been in the last 10 years (Display).

And in defensive industries, such as utilities and pharma, biotech and life sciences, share price gains last year were relatively modest when compared with earnings growth (Display). Multiples in these industries aren’t nearly as stretched as in other industries, so shares of companies with solid earnings growth potential are more likely to do well in a more volatile environment.

Evaluating earnings potential must take into account today’s unusual business conditions. In industries like retail or technology hardware, exceptionally strong demand during the pandemic and subsequent supply chain constraints may have inflated earnings and margins, which could revert to more normal levels as economic growth slows. In contrast, in some key defensive sectors, such as consumer staples and communications services, we haven’t seen these types of earnings distortions, which can help support more stable earnings patterns.

High Quality for Heightened Uncertainty

To find these companies, investors should avoid the market extremes—very expensive hypergrowth companies or extremely cheap low-quality companies. Companies that we call quality compounders have successful business models and sustainable earnings, backed by good capital stewardship and positive ESG behavior. These attributes support compounding earnings gains from consistent growth drivers through market cycles.

The volatile start to 2022 should serve as a wake-up call for investors. Extraordinary circumstances created by the pandemic have left many risks for investors to navigate. And global growth is also challenged by risks that prevailed before the pandemic, from populism and elevated debt to heightened regulatory risk and geopolitical risks.

But heightened uncertainty doesn’t need to be a deterrent from equity exposure. Focusing on defensive stocks with the right features and attractive valuations can help investors stay the course in equities through unpredictable times ahead and position to capture recovery potential.

ABOUT THE AUTHORS:Kent Hargis is Co-Chief Investment Officer—Strategic Core Equities at AllianceBernstein (AB).Sammy Suzuki is Co-Chief Investment Officer—Strategic Core Equities at AB. DISCLAIMER:The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

AllianceBernstein is an Associate member of TEXPERS. The views and opinions contained herein are those of the authors and do not necessarily represent the views of TEXPERS. These views are subject to change.

Follow TEXPERS on Facebook, Twitter, and LinkedIn for the latest news about Texas' public pension industry.